The Hot Blog Archive for April, 2015

Weekend Estimates by The Age of Kladaline

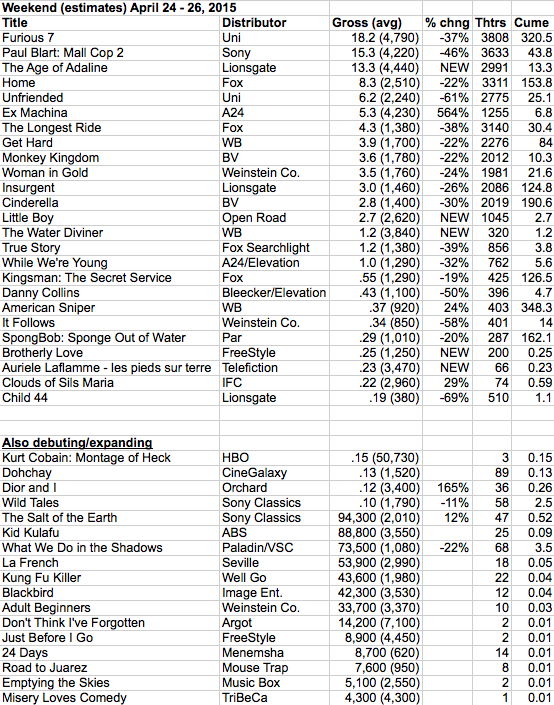

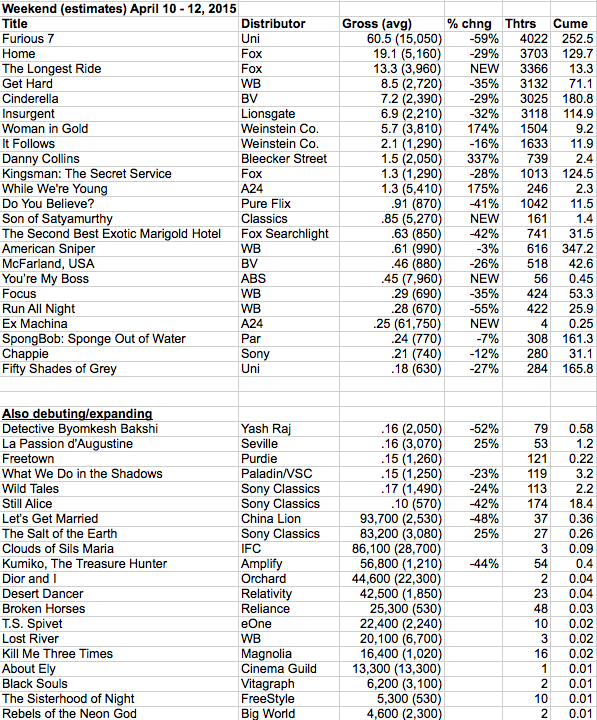

Nothing terribly interesting about the full weekend as opposed to the boring Friday numbers. The one truly notable thing is the strong increase for Furious 7 from the Friday number. The film is playing increasingly better on weekends against its Friday number. Opening weekend, it was 2.2x Friday, but that was loaded with must-see demand and Thursday late-night numbers. Second weekend was 3.2x Friday. Third, 3.5x. And now, 3.8x. Pretty unusual. Is the film playing to children? Is it playing as The date movie? Is this a function of women not being able to talk guys into going to Adaline on Saturday night but being willing to go to see vroom-vroom instead?

Anyway… The Age of Adaline turned out to be stubby-legged. Expect the number to be lower in “actuals.”

Blart and Home are benefiting from a soft family market, both holding well (one more surprising than the other). With only Avengers 2 showing potential for all-family viewing between now and Tomorrowland in three weeks, both should continue on positive paths.

Since the first Paranormal Activity, only once has the Jason Blum low-budget horror franchise failed to gross $32 million. No film has done over $84 million either. But that is the range (PA did $104m domestic). And everyone is pretty happy. Unfriended is the fifth film by Blumhouse for Universal. The previous four averaged $56m domestic each. Foreign on the Universal pictures is not as strong as it has been on the Paranormal or Insidious franchises, though it’s still another $32m each. So you do the math. $88m each on theatrical alone on a bunch of movies that cost under $10m each to make. Cautious marketing budgets means high profits, since that is the primary spend. Unfriended is heading to the low end of the Blum spectrum, but should still pass that $32 million mark easily.

Ex Machina is now the #2 film from A24 to date. But it’s not accelerating in any way that suggests it will able to hold screens for very long against summer competition. It was the #2 per-screen this weekend among wide-releases and will probably be #2 again next weekend, maybe #3 or #4. But there is a good chance that this is the top of the mountain. It’s just very, very hard to build something that becomes a “surprise hit” after it’s opened to bigger numbers. A24 has done – as Radius did with It Follows – an excellent job changing strategies fairly late and created indie-level hits. This will likely be A24’s top grosser before it’s done. But you look at a movie like Unfriended, which will probably do about twice the gross of Ex Machina, and wonder what a more mainstream release of the film would have looked like. Unfriended seems to have surprising critical support, but Ex Machina is a film that will live on for a long, long time. Would a wider release tarnish the love of the film by some (not all) critics? Would half the bigger audience hate it because they came to see a horror film and it turned out to be an intellectual piece?

Insurgent isn’t going to catch Divergent at the domestic box office, though it has done better than the first film internationally. But basically, a glass ceiling franchise at just under $300m a movie. Again… that sure seems like an attractive number… but what is the context?

Get Hard is yet another example of meeting reasonable expectations. Will Ferrell hasn’t had an original gross $100m domestic since The Other Guys (with Mark Wahlberg) in 2010. This movie is over $100m worldwide and will be somewhere around $90m domestically. That puts it in the Top 5 of Will Ferrell starring/co-starring live-action non-sequels. Yeah… it’s not huge and it has Kevin Hart, but this result is up to what should be expectations for a Will Ferrell movie. If it blew up, like Talladega Nights or Elf, that would be the gravy. But those are the exceptions, not the rule. $90m domestic being consistent is not mega-stardom, but it’s far from being nothing… especially if you aren’t making terribly expensive films. Get Hard‘s claimed budget is $40 million, which would include money to both Ferrell and Hart. That’s about what the ceiling on a Will Ferrell movie should be. And $25m with DL Hughley would be all the better.

Woman in Gold is another surprise indie story this year. That one seems sure to get to $30m domestic and do you know anyone who is not Jewish and/or over 50 who has seen it? Impressive.

And the per-screen champ of the weekend is Kurt Cobain: Montage of Heck, a Brett Morgan doc made for HBO and given a small theatrical that is packing them in. Mostly, it is a really good movie and for those who love the music, word of mouth has clearly made the theatrical experience a priority. As discussed repeatedly, there is the VOD glass ceiling to keep it from being too big a grosser. But for people who see death and destruction in the box office numbers, you gotta take your wins when they come.

Friday Estimates by The Klady Of Adaline

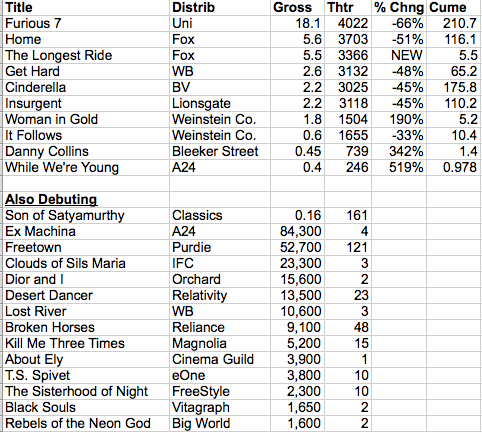

What a crap weekend at the box office!

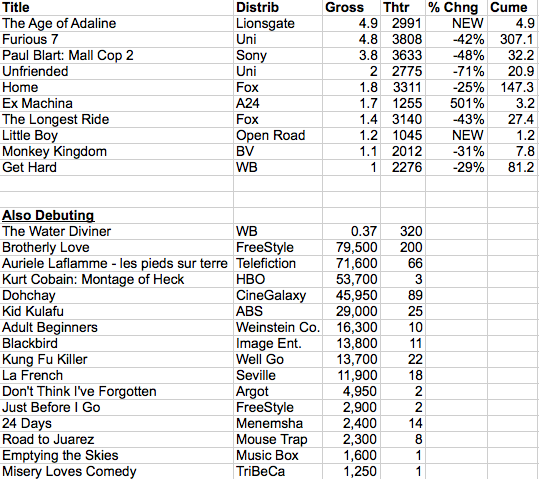

Lionsgate made a smart move pushing out The Age of Adaline here in the eye of the Avengers storm. It is not a hugely promising grosser, but it is counter-programmintog to next weekend and everyone else’s fear of being crushed gave it wide-open space for a single decent weekend.

Warner Bros played the weekend differently, sharting out The Water Diviner like a prisoner forced to pick a last meal. I wonder how much of the internal resistance to this film was a function of the hideous title, how much was that they saw it as an indie release, and how much was being unsure about whether Russell Crowe can still open a movie in the U.S. I have no idea, really… but it feels like all or any of those three notions could have been in play. In some ways, $3k per screen is a strong showing given that this one just fell off the back of the truck into 320 theaters.

Ex Machina‘s expansion from 39 to 1255 screens is one of those stories that can be unpacked a lot of different ways by the media. This weekend will probably come in just below the top weekend ever for young distributor A24, with Spring Breakers opening to $5.3 million on 1104 screens in 2013. But this is a much more accessible movie to a broader audience than was Spring Breakers. It’s a challenging sell, in that in order to get adults to go—who will like it, mostly, if they see it—you have to sell it one way and in order to entice under-25s, you have to see it a different way… and either sell seems likely to turn off the other demo.

In some ways, this is the Blade Runner problem. That film did good business for 1982 ($28 million, #27 for the year, comparable to Unbroken‘s slotting last year), but not exceptional business, certainly not in comparison to its footprint in film history. Why? It was a tweener. R-rated sci-fi noir, neither Star Trek nor First Blood nor Poltergeist. Ex Machina is, probably to its own team’s surprise, a tweener that could break out. I would say that last summer’s Lucy was a tweener that powered through with strong advertising and then, strong word of mouth.

The comparison that fits best, however, is not Lucy, which Universal pushed hard with a good amount of cash, but It Follows, which Radius realized had a potential good theatrical run in it at the last minute and pushed into theaters before dating the VOD. The expansion is almost exactly the same, screen-count-wise, though Ex Machina has beaten the IF grosses by a good margin. This weekend, Ex should do about 20% better than IF‘s third weekend expansion to 1218 screens. The big test will come next weekend, #4, which is when It Follows expanded and still lost forward momentum at the box office. Will the same happen to Ex Machina or will it ascend? The conservative estimate would be that Ex Machina ends up with about $16.5 million at the box office. That would still make it A24’s best grosser by a good margin. But will Avengers and then Mad Max get in the way? Will word of mouth carry the day? This is the challenge for A24.

Also having a happy weekend is Brett Morgan, whose Kurt Cobain: Montage of Heck is doing bang-up business on three screens, heading towards a field-leading $50k per screen for the weekend. It’s a really good movie and there is no better way to see a music film than in a theater with great sound. What better way to come down from Coachella than with Kurt Cobain at the movies?

Finally, Furious 7‘s holds continue to be quite good. Is it the film, the success or the lack of competition in this month’s marketplace? No idea. And Home‘s is also holding well, still right in line with How To Train Your Dragon 2 for the hit-hungry DreamWorks Animation.

23 Comments »Review: Avengers: Age of Ultron (1 marked spoiler… at the end)

I spent a surprising amount of time during Avengers: Age of Ultron thinking about my age. I saw what Joss Whedon was trying to do, but the film was so obvious in its ambitions… so episodic… so lacking in genuine surprise… that I found myself wondering whether others around me were having the same experience or whether I had hit an age where I just don’t have it in me to give myself over to a movie like this.

But as the movie continued, I realized that it wasn’t just me. The film feels like the work of a filmmaker trying to fix his perceived flaws from earlier work. But it also feels at one with the general movement of Marvel as a content producer these days, as seen in Captain America: The Winter Soldier and “Daredevil,” made for Netflix. More and more talktalktalk, punctuated by action sequences that are sized to fit the budget of each project. But the chatter has become more and more insipid as it reaches for profundity. I know some of you bought The Winter Soldier‘s ham-fisted ambitions to pose as a 70s thriller with a comic-book movie laid over the top. “Daredevil” repeats fairly simple ideas to the point of exhaustion, coming alive only in its martial arts-y action sequences (which also get repetitive ) and anytime Vincent D’Onofrio shows up as Wilson Fisk (whose origin story the show really is about and who doesn’t get nearly enough to do).

In Ultron, the Avengers are a well-established family. Inside jokes, established expectations, familiarity over competition. The group is so dominant that the screenplay has to dig into the classic tripe of making fun of what is obvious, particularly the idea of anyone shooting a gun at a super-being and the fact that the two Avengers not imbued with superpowers are mortal. In fact, I cringed a little every time I saw a cadre of guns aimed at the supers, whether by human props positioned as bad guys or as good guys. What is in it for us as an audience when people shoot guns at Hulk? I don’t get it.

In any case, Avengers feels like a third or fourth movie in a series. And thinking about it the morning after, that feels right. After all, we have had two Thors, two Caps, and three Starks. The characters are tired, no matter how much we like them. Even the casting feels tired. Excuses about the absence of even cameos by Gwyneth Paltrow or Natalie Portman abound, though the characters are discussed. And there is a former-SHIELD switcheroo that feels like two actors are playing one role, but one of them couldn’t find the time to show up for half the movie, while the other disappears completely and without mention in the second half. What the hell was that? And when the first former SHIELD-y is in the film, it feels like some sort of gender balancing choice… which I wouldn’t object to if it weren’t for the fact that she gets almost nothing to do but spout jargon and look good in a skin-tight dress.

The exception, with the core group, is Hulk, who finally got to break free the way everyone seems to have wanted him to in the first Avengers. And while not as heavy and pendulous as the two Hulk movies, Whedon really loses the Hulk joy in this one. I won’t spoil anything, but I will say that the audience does not get what is promised and desired from what is (endlessly) set up in the story.

And then there are the new characters, Scarlet Witch, Zippy The Fast Boy, and Ultron. Oh… wait… Quicksilver… sorry. Unfortunately for Zippy, the really good Quicksilver speed gags were kinda used up by, uh, Quicksilver, in X:Men: Days Of Future Past. So our Quicksilver suffers thrice for this, primarily with an unclear role for his power, secondarily with a recurring gag that doesn’t really play, and (removed for spoiler). Scarlet Witch – not to be confused with Scarlett Johansson though they make sure we get a lot of her cleavage though they shoot away from her lower body often because she does her fighting in short skirts – has a role and powers that grow through the film, though again, she seems more powerful than her CV suggests at times and then very limited in her powers. This is one of the inherent problems with superhero films, which is filled in by your mind when reading a comic book. The degree of destruction from any one-on-one battle makes the return from a two-minute jump to what other characters are doing feel like we missed another whole city being destroyed.

And then… Ultron… who is not quite what we were sold in the ads. I understand the choice to make his mouth move when he talks, but it makes him look comic, almost like the Scarecrow in The Wizard of Oz. But his central conceit is a bit simplistic, really… at least for a character who seems like he could be really interesting. And the execution of ideas basic to the character – that any physical embodiment of Ultron can be destroyed and he just skips to another robotic body – just isn’t very good. I mean, we went here with The Hidden on a million-dollar budget in 1987 and it was brilliant. Here, it’s just ill-defined and confusing. I mean, I figured it out and all, but it isn’t done so the audience can follow it and track it. What are the hordes of robots for? Are they fighting the Avengers or are they just replacement parts? There was a great opportunity for cleverness and poignancy in this idea, which is in the film… but it just doesn’t play.

And that really is the big picture review of this film. It’s everything as well as the (very dangerous) kitchen sink. Whedon is reaching for so many things that even when he doesn’t miss (and 90% of the uber-serious dramatic dialogue is awful), he undercuts what could have been great fun by throwing too many toys into the playpen at once. “When everyone’s super, no one is!”

And don’t get me wrong. There are conceptual improvements. The final siege on a city is not as simplistic as the attack on NYC the last time. But… it’s still a city attack with a lot of undefined bad guys and a lot of time spent herding humans to safety.

Less would have been more.

You’ve all seen the giant Iron Man vs Hulk in ads and stuff. Well, that – like much of the other action – felt more obligatory than story-driven. They just needed a way to up action. And yeah, there is some cool there. This is not a horrible movie. I’d say there were three or four moments that really sparked for me. But the density made what was so clearly not formulaic still feel formulaic.

And here is my spoiler bit… because I think it is really a critical notion…

SPOILER

SPOILER

SPOILER

One of the best elements of the film is the introduction of Vision… which happens in the third act. How it happens is a convoluted mess that Stark tries to explain… but it’s just not believable… but of course, in the end, who cares?

Basically, Vision is Stark’s best idea of Artificial Intelligence, as literally embodied by Jarvis, his digital sidekick through all of his films and The Avengers. Ultron is the version of A.I. that he didn’t mean to launch and, basically, escaped.

The problem with Vision showing up at the end of the film is that we like him better than almost anyone else and we don’t get much of him. He has no chance to develop relationships with the Avenger characters. And the end of the films suggests that he never will. That’s unfortunate.

But the entire film could have been much better had Stark launched Vision from the start… then Ultron created himself from the scraps, a gag they use in the film, but much more poignant if he starts out that way… the Cain to Vision’s Abel… the younger brother with a giant chip on his shoulder. This would have also solved the motivation-for-Ultron problem. Ultron wants to destroy human life because Vision values it, not because Tony Stark made some overheard passing comment while talking to Banner. And even better, we would have seen how Vision comes of age and interacts quirkily with all of the characters we already know.

And as long as I am in a spoiler space… come on, Joss… get on with it. The audience doesn’t want to watch Banner pull a Spider-Man “I can’t have love” drama on Black Widow. They want to see them get together. This movie has more filler than Zsa Zsa Gabor’s face. (alt obscure reference: Ken-L-Ration) No one really cares about Hawkeye, much less his wife and kids… were you kidding with that? There are striking images to be mined in superhero hallucinations… but probably not five in one sitting. Too much!

And one last thing… the Hulk/Iron Man fight ending… no.

SPOILERS OVER

SPOILERS OVER

SPOILERS OVER

We would have been better off with the hour-forty version… though that isn’t true because the way the movie was structured, it can’t be cut down very easily. So we would be better off – albeit bored to tears – with the three-hour version. It was like Whedon thought about the first film and felt like it wasn’t deep enough, not realizing that its success lay in its comic book shallowness. It was just fun for audiences.

And there is fun in Avengers: Age of Ultron. But it’s like sitting through a long conversation with someone you are desperate to borrow money from… all you really want is for them to lend you the money so you can relieve whatever discomfort that money will fix. But they need to tell you about why you shouldn’t be borrowing money and how important it is to be responsible like they are, etc, etc, etc. You just want Hulk to smash Loki again.

But alas, the grasp is beyond the reach.

64 Comments »Comments

Sunday, 4:30p – We still don’t know why, but comments seem to have been broken since Friday afternoon. Sorry. Will let you know when it starts working again…

Sunday 4:48p – Comments are working again. Apologies for the inconvenience.

Weekend Estimates by Ex Kladina

An interesting weekend for a change.

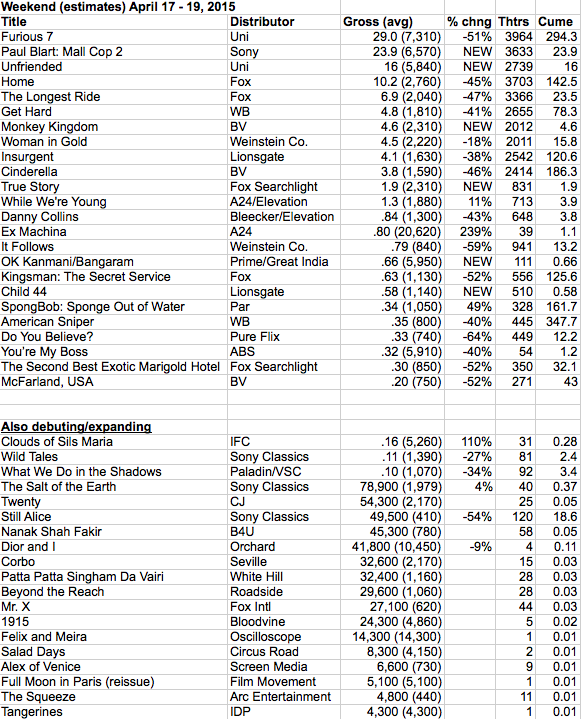

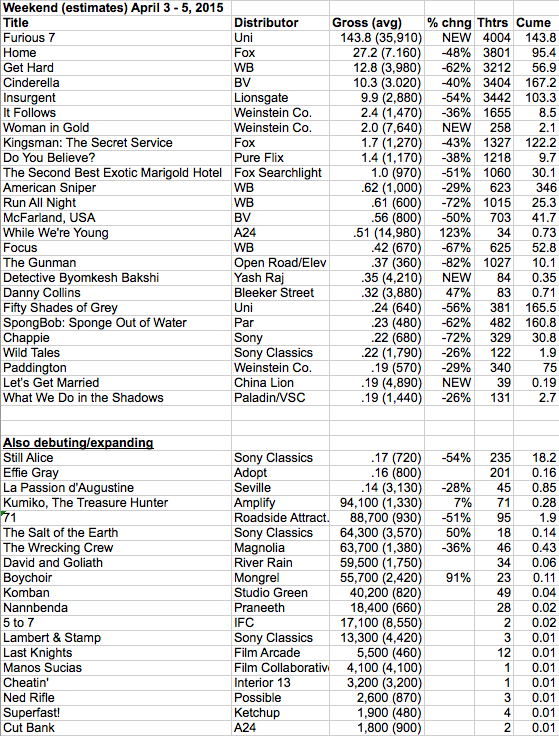

Even the Furious 7 is interesting at this point. A mature franchise leaping somewhere around 60% in gross.

Or maybe it’s a little more obvious than that. The racial thing is not new. Paul Walker, however good a human being, was not a big worldwide box office star. But they have been selling this as “the last ride.” And Walker certainly had fans in the context of this franchise. Let’s assume that these factors could tweak the significant incremental growth of the franchise from 4 to 5 to 6 to, now, 7. The last 3 films had each grown in box office at a rate of somewhere between $125 million and $175 million worldwide.

And then there is a panda in the china shop… China. From what I can tell, Fast & Furious 6 was the first film to get a theatrical release there, in 2013. About $70 million. This one, their second? $250 million and counting. International growth outside of China? A bit over $50 million (to date)… or right in line with the previous growth of the franchise.

I am not a big fan of box office asterisks. Don’t like counting tickets (especially because the historic counting available to us is impossibly flawed)… don’t like adjusting for inflation. There is no logical comparison between box office in the 30s, 40s, or 50s, and box office now… forget about all the other availability like DVD and streaming and distractions, just on the basis of TV, the mass audience lives with movies in a very different way. The industry adjusted to this, but ticket counters don’t seem to get it. The past should be honored, but it is not an easy comparison.

But my point is, Chinese box office demands asterisks. On the most surface level, it is 3D in reverse… but it bends the box office conversation even more than 3D because all of the revenue is the same, much small “rentals” than anywhere else. Studios receive less than half of the box office take compared to anywhere else in the world. So, effectively, the grosses from China are worth (less than) half of what any other reported grosses are worth to the distributors. It is still a massive, growing, absolutely critical market for Hollywood. But there are now 20 billion-dollar-plus films and Furious 7 is just the 5th one of them to have gotten over $100 million added to their box office by China. And the onslaught is coming…

Another film that is about to move from the marginal China revenue category to maga-bucks is Avengers: Age of Ultron. The first Avengers, the first non-Jim Cameron film in history to pass $1.35 billion at the box office, only took in about $86 million from China… not nothing, but not a critical amount in defining its success. The cast is currently in China, promoting the sequel, and I can’t imagine that it won’t lead to at least $300 million at the Chinese box office next month. This could push the film close to the $2 billion mark, heretofore only cracked by Titanic (in 2 releases, including $45m from China in it’s digital re-release) and Avatar ($204m from China… the first Hollywood mega-gross in the country, in 2010).

Does it matter? As I noted at this beginning of this rant, I am not a big believer in asterisking every bump in the box office road. But unlike, say, 3D, access to the Chinese audience is not open territory. Not everyone can play. And if the grosses from China are 27% of a film’s title worldwide gross, meaning that the distributor will receive around 15% less from their worldwide gross, that is pretty significant (this is the story with the last Transformers movie).

And in 20 years, this will probably look like just another bump in the road. China will show more Hollywood films. More revenue will be returned to distributors. We’ll start seeing annual grosses over $500 million from China. It’s all gonna happen. Fair enough.

And there are plenty of surprises in this growth. You might assume that a mega-hit like Frozen made a killing in China. But no. Only about $50 million. It did 5x that in the mature market of Japan. The 10 Hollywood films that have done over $100 million in China, to date, are Furious 7, Avatar, Iron Man 3, Pacific Rim, Interstellar, Dawn of the Planet of the Apes, Captain America: The Winter Soldier, X-Men: Days of Future Past, and the last two Transformers movies. That’s it. These are early days. And unless we can get a handle on piracy, it may be the last big market to go into play.

But for now, we should all have an asterisk in our heads when chewing on these numbers. But more importantly, we should be conscious of the “magic trick” that seems to be happening in front of our eyes. And as grown ups, we also have to be able to balance the questions about domestic box office – which has been shrinking marginally on an annual basis for decades now – and international grosses, which represent 95% of the population of the earth.

But I digress…

Paul Blart: Mall Cop 2 had a good opening, which only looks weak when compared to the release of the original, a surprise hit. But after 6 years, Blart ain’t exactly Star Wars coming back. Sony should be thrilled that it’s only off 23% so far.

Unfriended is yet another Jason Blum film… low budget, decent box office = profit. If you want to examine how power works in Hollywood, follow the Jason Blum. He is the kind of asset that can make a career in this town. A money tree. For now. (This trend will eventually pass and Blum has shown a broader interest than just horror/thrillers, including Whiplash, but that will be his 2nd act.)

I am glad that Disneynature exists. But Monkey Kingdom is one of those films that makes one worry that it all may get shut down before long. Really, Disney can lose small amounts of money on the films and keep it going just in brand support of its animal theme park interests. And you never know when one will shock everyone and hit big. Anyway… soft opening… not a disaster.

True Story isn’t a pretty launch. But it’s not a pretty movie. Life will go on for Searchlight.

And Child 44 was thrown out into the world by Lionsgate like an unwanted child. Audiences responded in kind.

But back to the happy stories… Ex Machina expands from 4 to 39 screens and scores a $20,620 per screen average. That’s really good. It doesn’t guarantee a huge gross, but it suggests that this could be A24’s biggest film. They are approaching it with a lot of caution, for better or worse. But the buzz is clearly growing. If you look at the other indie genre hit on 2015, It Follows, the 2nd weekend expansions are of a similar size (39 vs 32), but Ex delivered about double the per-screen, even with the higher number of screens. It Follows is at $13.2 million and A24’s high grosser so far is Spring Breakers with $14.2 million. So that seems doable.

Looking for a higher end comparison for Ex Machina, I looked at Birdman, which had slightly better numbers in expansion ($27.6k per on 50). Then there is Chef, which never had these numbers, but played well for a long time. Both of these films had the advantage of adult audiences. This is the dichotomy, as Ex Machina should do sensational business with genre fans, but is a smart film that could also play to grown-ups who usually eschew genre. A24, which is also having some success with the dramedy While We’re Young, is very into smart tweeners. If they can continue to build on their commercial success, they could become the next great light, leading the way in the indie world.

Also having a nice weekend is the Dior & I team, which is running a little behind Valentino: The Last Emperor, but is looking like it will be a million dollar doc, which is a not-insignificant challenge these days.

Also doing a strong per-screen number, albeit only on 1 screen, is Felix and Meira from Oscilloscope.

The glorious Clouds of Sils Maria, which seems to be more divisive for audiences than it has been for critics, did an okay $5260 per-screen on 31. This is one of those cases in which IFC eschewed day-n-date VOD and isn’t seeing it pay off in a significant way.

8 Comments »

Delivelution: April 2015 – Pt 2, Meet The New Bundle. Same As The Old Bundle

Gosh darn, the media luvs change. Any kind of change (aside from losing their particular jobs). Gotta have it. Reporting “nothing has changed” or ” there has been incremental change” isn’t very exciting.

Almost four-and-a-half years ago, ESPN started streaming its networks live. For an even longer time, the sports programming leader has made programming that didn’t make it onto the networks available for streaming and PPV.

Another Disney television network, ABC, has been streaming their programming for almost two full years.

So why don’t these leaders in emerging media technology seem to ever get mentioned in stories about the future? Because they aren’t cord-cutting tools.

Now, as ESPN streams on Dish’s extremely limited streaming Sling TV network, suddenly they are a part of the conversation again… but only as a part of the cord cut.

Let’s process this… Disney makes their ABC broadcast network available to stream to scores of millions as a free part of their cable/satellite (MVPD) subscriptions and… not a story. But Viacom’s CBS makes their network available to a couple hundred thousand (maybe) cordcutters for $6 a month and BOOM… the world is changing.

If you want to follow a niche group that likes to pose and whine constantly, feel free. But that never ends up being the story.

One journalistic axiom that I live by is “follow the money.” And the story here is about what will happen when 80 million+ households are ready to take action.

There is no cliché more worn out that “everyone wants what they want when they want it and they want it for free.” Yet this is how the evolution of content distribution is constantly covered. Make no mistake, there is an evolution going on. The vast number of ways that content will soon be distributed constitutes an immense change.

But here is what has not changed, and won’t change. 60 seconds in a minute, 60 minutes in an hour, 24 hours in a day, 168 hours in a week. The vast majority of people will spend 35-56 hours of every week sleeping. That same majority will spend between 20-60 hours productively working (inc school, etc) during most weeks. So what does that leave? 20-60 hours a week entertaining ourselves in some form? Food, sex, bathing, thinking… all eat into that.

And the value of money will change, but people will basically make similar amounts now and 50 years from now. And no matter how excited the press gets about change, until filmed entertainment can fully replace food and/or drugs and/or alcohol and/or sex and/or sleep, the average American household will not be spending a lot more, by percentage, on these things than we do now. $250 – $350 a month is about the cap.Of course, on the high side, that adds up to over $400 billion a year. The question is, how does it get cut up?

Now… let’s discuss the bundle.

As soon as you put a second piece of entertainment together with another to increase value, you have a bundle. Netflix and Amazon and Hulu are all bundlers. They bundle content with the idea of appealing to the widest possible group, few of whose tastes will match consistently through their viewing. Meaning… if one-third of the Netflix subscribers watch a show like “House of Cards, “that’s a huge win for Netflix, as they have created unique value for one-third of their buyers. Maybe another one-sixth subscribe for old TV shows. Another one-sixth like the range of docs available. Maybe one-third can’t live without the kids’ programming. Etc, etc, etc.

This is also the kind of bundler that the major networks are, except that their targets are even wider. They get paid based on how much everything they air gets watched, not by subscriber purchase and loyalty. Also, they have historically lived with the limits of the 168-hour week or more to the point, 22 weekly hours of primetime and a wide variety of daytime and latenight chunks. So, for instance, today (Monday) on ABC, the network will program, on most affiliates, 16.5 hours of the 24 hour day. On this upcoming Sunday, they have 12 hours of programming. Fox, on the other hand, will only program two hours of the 24 hour day of its affiliates today (Monday).

MVPDs (cable/satellite) are a third form of bundling, pulling together an attractive series of networks to reach an audience even wider than the broadcast networks. These companies were tasked, at the start, with serving the communities to which they were given exclusive rights on a town by town basis. Local stations were included under “must-carry” rules. Networks like TNT and USA used major league sports to make them semi-unofficially must-carry (as in, you need to have them so your constituents can see their local teams when they are televised nationally).

Bu things changed dramatically as (and there are lots of pieces, but sticking to my point here) the MVPD world solidified and what were specialized networks realized that they could compete with the more mainstream cable networks and even the broadcast networks. Cable nets like MTV and Bravo and AMC and History realized that they had 70 million-plus (many of them around 100 million) potential viewers to work with, same as the major broadcasters had sole access to for years. Why program only niche shows hoping to find hundreds of thousands out of an interest group of a few million when they could shoot for millions of viewers.

And as those higher pursuits expanded (along with the costs), those networks grew more important for those MVPDs to keep their subscribers and the shoe changed feet. Now the networks had an advantage (as did ESPN and other older nets). But there were the broadcast networks, who still draw more viewers overall than any other segment of the MVPD content universe, spending lavishly and creating hundreds and thousands of hours of new programming annually and not getting paid by the MVPDs. And so, that shifted and now they are – for the most part – being paid to be available via your cable or satellite provider.

In other words, your cable company started paying a la carte prices to hold together your bundles, all the while listening to you, the consumer, complain about 500 channels with nothing on.

Is this the only reason your cable/satellite bill has been steadily/sneakily rising over recent years? No. But it is a big part of the cause.

So now we get to cutting the cord.

If you just say, “Man, I don’t need all of that!,” God bless you and opt out of this conversation now. You are part of a very small group of people who are just fine making that leap. Congratulations.

As for the rest of you… your decision is really about choice. There is expense. And there is easy, wide-open access. And there is the vast space in between.

Here is what is not going to happen… you are not going to get to pick the channels you like and only those you like and shave 50 cents or a buck off of your bill for each one you eliminate.

On my DirecTV, the first 70 channels are committed to local “free” TV. 70 – 100 are all shopping channels. 101-200 are all DirecTV PPV or other in-house programming. 201 – 221 are news and sports channels (some very specific, like The Golf Channel). More shopping from 222 – 230. 231 – 288 is the meat of the cable programming… Food Network, Bravo, AMC, E!, History, Discovery, FX, A&E, Comedy Central, Lifetime, Oxygen, WE, Oprah, USA, TNT, TBS, etc. Kids programming 289-304. A bit of a mash-up until MTV at 331 which starts music and hip entertainment until 345. News channels from 346 – 360. Religion 363 – 379. Unavailable national nets from 380 – 400. Spanish-language nets from 401 – 462. DirecTV space until HBO and the premiums nets at 501, which go until 573, which is when the porn starts. The 600s are for local sports networks. The 700s are for paid access to sports. 800s are music channels. Everything 1000 – 2000 is now on-demand channels. And over that, it’s DirecTV inside baseball.

So what do I use? Not the 70 channels of free TV… but the ones I want and the others are free to me and DirecTV anyway. 201- 221 are sports channels I watch. 231-288 are core. The news channels are important to me (346-360). With a kid in the house, the Kids nets are important (289 – 304), even though he also uses Netflix all the time. I don’t watch much MTV (331-345), but it would be weird not to have it available. And the premium channels, which I am already paying for at great cost.

So… with a roughly 500 channel “basic” universe on DirecTV, I care about roughly 120 channels. Within that I could surely pare it down to under 100 channels… maybe 75. But as I wrote before… it doesn’t work like that and will never work like that.

Still, even with a priority of 75 channels (before premium nets), there is no way to achieve that bundle solely by streaming.

Rumor has it that the Apple offering will be around 50 channels… but what 50 channels?

And each of us (who do care about having a fairly broad level of access) will have to ask ourselves, what is our tipping point?

What level of inconvenience is $50 a month worth? $25 a month? $75 a month?

And this is where is becomes a giant cluster f***, because as we seek to break the bundle, we each become responsible for creating our own bundles. And that includes making sure your internet access through your home works well enough for streaming consistently and with minimal interruption.

I’m not playing the “what’s available right this second” game here. I’m taking the Playstation Vue (now in 3 cities) and the reporting on Apple to be mostly accurate. (Sling TV, as far as I am concerned, is already dead. 20 stations, no broadcast… not going to cut it. In time, it will get the networks. It will have to in order to have any chance. But it may well be too late.)

Playstation Vue is offering up to 88 channels. But the offering changes in each of the 3 cities in which Vue is currently available… and again based on the three levels of service. In all 3 cities, the cheapest level, “Access,” is $49.99 a month. In NYC, you get 53 channels at this level. For news, there is CNN, HLN, Fox News, Fox Business, CNBC, and MSNBC. For sports, there is Fox Sports 1, Fox Sports 2, NBC Sports Net, and networks that show some pro sports, TBS, TNT, CBS, NBC, and Fox. No ESPN (on this or any level). And no ABC (on this or any level). To get YES (to watch The Yankees), you have to go to the “Core” level, which makes it $59.99 a month. For kids, Nickolodeon, Nick Jr, and Nick Toons. No Disney (on this or any level).

And what about the “meat” channels I referred to earlier? Not bad. AMC, Bravo, E!, Food Network, MTV, VH-1, TBS, TNT, TCM, TLC, USA… all there. But A&E, BBC America, History, Lifetime… sorry. And logically, if those channels were to sign on, it would be another tier of $10 a month for their inclusion.

The $69.99 “Elite” level is a load of 21 unnecessary channels. If you feel strongly about having Logo (the most surprising channel to be held Elite hostage, because it seems like a political misstep) or Boomerang or The Cooking Channel, so be it. But you pretty much get it all for $59.99… but with some big holes. Add HBO Now and you’re up to $75 a month. Add Netflix, Hulu and Amazon Prime and you’re just over $100 a month. Without a DVR. With limited video-on-demand over a tightly limited period. Without a number of significant networks, including premium nets Showtime and Encore. Currently, PS Vue doesn’t stream to the iPad or iPhone, but they say that will soon change, so I won’t hold it against the service… and I will hold it against DirecTV and other MVPDs that don’t allow much live streaming of their top networks outside of the home.

But… it’s just another bundle. And even at the “Core” level, did you really ask for the Cosi Channel, Destination America, the Big 10 Network, Esquire Network, Animal Planet, Science, Discovery Family, TeleXito, etc? I’m sure some of you wanted one or two of them, but these are the networks that are noted as “unneeded” when people complain about MVPD bundles.

If I could get this for my wife’s parents, in their 70s, who rarely change the channel from Fox News, and wouldn’t worry about not having ABC or ESPN, my inclination would be to say, “sold.” Of course, they would need internet service, which they might choose not to have. They still pay all of their bills by mail.

Unfortunately, checking in with Time-Warner Cable in my neighborhood, they could have 200 channels (100 in HD) on 3 TVs with DVRs and the internet for $129 a month. Or they could pick 20 channels on 3 TVs with DVRs and the internet for $80 a month.

Now the value proposition is razor thin, at best.

The irony of all of this is that the people most anxious to cut those chords and lead the revolution are younger… and The Young are the group most focused on event moments, whether the newest TV episode or movie. Older people tend not to be as must-see focused. They are willing to wait to consume their entertainment. They don’t feel compelled to jump on Facebook or Twitter to discuss something minutes after it ended. But those younger people are happily throwing up release date hurdles for themselves and the older audiences are less willing to go through all that effort (or multiple delivery systems).

But returning to the central point of this episode… “bundle hatred” is a false premise used lazily to express the disaffection for the current, overly mature system of local near-monopolies that have lowered the bar on the need for MVPDs to aggressively service their customers in a positive way.

Many consumers (perhaps a majority) feel like their content delivery systems are too expensive and not worth the price these days. They see a load of channels in their cable/satellite guides that they never watch. And they figure that if you just trim the fat, prices will go down. They also want maximum access to content on digital platforms.

I believe that consumers will end up winning this battle, as they mostly have so far. But it will not be the revolution of which many dream. If you want to reduce down to local TV by digital antenna and the 4 big streamers (Netflix/HBO/Hulu-Plus/Amazon Prime), you are good to go for under $100 a month (including internet) for as long as the broadcasters are putting signals in the air.

But if you want to consume with some abandon, $150 – $200 a month is likely to remain the norm for a long time to come. What I see coming in a lot more content for the same overall price point. Some networks will die. MVPDs will be a part of the machinery, but will earn a lot less revenue from content sales than they have, focusing more heavily on providing internet services (as many have suggested before me).

The need to have multiple networks, like six HBOs, will dissipate. NBCUniversal has 15 of the 88 Playstation Vue channels (and a similar or bigger clock on MVPDs) currently. Occupying channel space has been a leading strategy for 20+ years, but having – for instance – both Cloo and Chiller in a digital on-demand universe seems redundant moving forward.

So maybe the bundle will only have 20 “channels,” each channel priced at various levels. But there will still likely be basic and premiums levels that cross all those channels. The difference from now is, you will be able to watch what you want wherever you want to, the DVR will be phased out with access to download any post-release filmed entertainment (and perhaps be broken into multiple windows, but not ones as seemingly arbitrary as right now), going to movies will be about that very specific experience which could well be as popular if not more popular than now, and television will fight for a few million viewers from across the globe on the nights of premieres and far more in the 2 – 3 weeks to come.

But I am getting ahead of myself. More to come…

Part 1: Unscrambling Eggs

Part 3: The Tyranny Of The Old

Part 4: $200 Billion Is Never Enough

Weekend Estimates by Furiouser

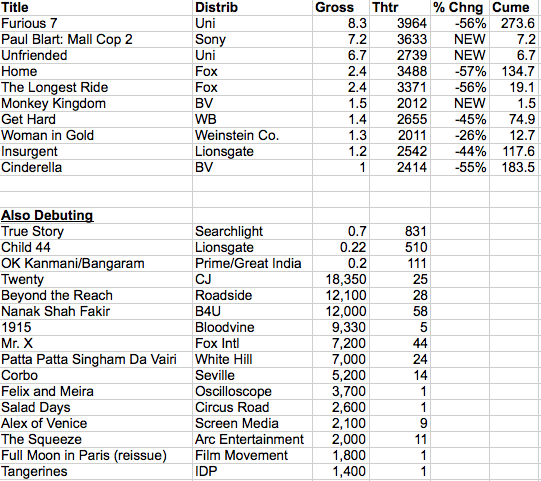

Not a very eventful weekend. The Avengers 2 junket got more media attention than any of the films in release.

But a solid hold for Furious 7. The film’s domestic lead over its predecessors in the franchise continues to expand week by week, which is impressive. Just tree weekends in, this is already the highest grosser of the series, with literally hundreds of millions (2) still possible worldwide. I didn’t think a billion was possible… but it clearly is at this point.

Home is actually running ahead of How To Train Your Dragon 2 right now. Beating the domestic number would be a very positive event for DWA, especially given that Dragon was a sequel and it was a summer film. I doubt that Home will come close to Dragon 2 internationally, which speaks to the ultimate profitability. But if it comes close, that’s still a big win. That would give DWA winners at Fox for three years in a row: The Croods, Dragon 2, and now, Home. It would also kick current thinking in the teeth… that familiar brands are the best way to go. If DWA can keep producing one new strong, original franchise player a year, it could quickly put Rise of The Guardians (Santa, Easter Bunny, etc), Mr. Peabody & Sherman, and the spin-off of Madagascar in a different light.

The Longest Ride simply failed to hit the marks (Nicholas Sparks meets Nashville) it was seeking. It is by no means a disastrous opening. Just not a great one.

Insurgent is now, officially, a mature series. The number ain’t going to change much on the last two films… domestically. But there is still some hope for real growth internationally. Indications are (someone will kindly correct me if I am wrong) that there are a lot of territories out there to still open and Insurgent is already close to Divergent‘s international total. If Mojo’s charts are accurate, high- grossing countries like China, France, Germany, Russia and Mexico are all still untapped and international could add another $100 million before its all done, taking the franchise to or close to the $400m worldwide mark.

Indie expansions are getting a lot of play this month. $5.7 million for the weekend and a cume coming up on $10 million seems like a ton for Woman in Gold, a Nazi artwork-return drama. The expansion of nearly 6x the screens of opening weekend led to just under 3x the opening, which is a very solid number.

Also from The Weinsteins, Radius’s trend-setting choice not to day-n-date It Follows continues to pay off. Our estimate for this weekend is much higher than some, but whether the film is down a little or up a little, the numbers are very good… under the circumstances. With word-of-mouth like this, it makes you – or it should make you – wonder what would have happened had this been released in a normal way and had a bigger initial sampling group. I am glad that this opportunity was not squandered by Radius… but we are heading to the next iteration of indie distribution, where opportunities like this – great movie, great critical acclaim, popular genre – are never day-n-date VODed and that bigger theatrical distributors are more anxious to buy these kinds of films. Radius is a terrific company, but they have had quite a few films fall into their VODing hands that were really strong commercial plays. These have been some of the most successful VOD films… but could have been more.

The trend set by Radius is seen with Clouds of Sils Maria, a truly great movie that IFC is releasing in theaters without a VOD date set, much less launched on the same day or within a week. The result this weekend was a strong $28,700 per-screen on three (by estimate).

And Danny Collins, from first-time distrib Bleecker Street, has taken its time and is seeing some payoff from their seeding of the film. Pacino’s made four “small” films in a row (Stand Up Guys, The Humbling, Manglehorn, and Danny Collins). The Humbling had a messed-up run at award season and might comeback theatrically… we can hope. Good movie. Barry Levinson directing. Buck Henry script. Stand Up Guys didn’t do much. IFC is bringing out Manglehorn, but that strong David Gordon Green film will challenge audiences in a commercially unfriendly way. So it looks like Danny Collins will be the top grosser of the group. Pacino is having a career resurgence thanks to his daring, interesting choices. I hope audiences will get to see it.

Also continuing to expand well is While We’re Young from A24, adding about 8x the screens and doing about 3x the gross. Solid against the expectation on these kinds of expansions.

A24 also has the most excellent (and most horribly titled, for commercial purposes) Ex Machina, which did an estimated $61,750 per screen on 4, behind only Spring Breakers in the distributor’s short history. This is another film, like It Follows, that feels like it could have been a lot bigger with some more marketing firepower (read: money) behind it. I will try to find out the story behind Universal selling domestic rights to A24, because it seems like someone over there blew the pooch on this one.

Also in exclusive release, documentary Dior and I did an estimated $22.3k per on 2 from Orchard.

13 Comments »

Delivelution: April 2015 – Pt 1, Unscrambling Eggs

Pregnant again.

Before film, all moving entertainment content was live. Movies were the first born. It took until 1951 for television to be birthed for a consumer audience. The Delivelution had twins in 1976 with the first national cable networks and the launch of commercial videotape player/recorders. Baby 5 was commercial DVD in 1997.

And now, streaming.

We are still in the first trimester of What’s Next for the content delivery business. But we can expect the baby to arrive with most of its fingers and toes in a couple of years, with surprising symmetry, 20 years after the launch of sell-thru DVD, as DVD came about 20 years after VHS and VHS 25 years after broadcast TV.

Of course, I have left out a lot of the detail work in between these “children.” The Internet, for one. But this is not unintentional. The coverage of the Delivery Evolution of content tends to get caught up in those “trees” and to lose view of the “forest.”

The phase we have been in for a couple of years and will continue in for a couple more is an unscrambling of the content eggs.

For almost 40 years, cable has been at the foundation of post-theatrical content revenues. And the industry has built and torn down infrastructure over that entire period, seeking maximum revenues. Cycles have repeated endlessly. Empires have been built and burned. But it terms of the broad strokes, pretty stable. As a result, cable companies that were already wiring homes, were able to build a second arm of their businesses wiring the internet into those same homes. And some became content players. Vertical builds became all the rage. The world was being reduced down to a handful of mega-businesses.

But while there is an element of that still going on, something changed a few years back. These giant conglomerates realized that they were not maximizing revenues anymore with everything under one roof. The savings attached to being consolidated were less than the perceived potential earnings of smaller, more lithe units chasing maximized revenues.

Meanwhile, in The Delivelution, content library values were bottoming with the DVD ownership business. DVD went from being a massive added-revenue situation to being integrated into steeply rising costs of production and marketing and when it hit the wall, it was showing signs not just of maturation, but old age. Pricing had become so low and sales so high that people who were buying out of habit were looking at piles of unwatched, valueless DVDs. Moreover, Netflix came along with a cheap rental solution that made ownership seem silly for many consumers.

So where was The Money? Back to the cable companies. Around $100 billion in gross revenues annually on the cable/satellite side alone. Content costs were relatively low. And so, content providers started to squeeze. And so began the post-DVD second generation The A La Carte Era.

I am simplifying, but for the purposes of this column, forest, not trees.

And so… now we are in the period in which everyone is trying to unscramble their eggs and to sell them much more carefully than they had over these last 40 years of relative post-theatrical stability.

My date for the start of this era is June 9, 2009. That is the day the SAG contract with AMPTP was overwhelmingly voted in by SAG’s members. The agreement with SAG, under the claim that there was little-to-no money in the “emerging technology” of streaming had cleared a number of cost hurdles for the content owners and buyers.

Hulu, initially a partnership between NBCUinversal and Fox with Disney coming aboard in 2010, started streaming reruns in 2008. The 2009 SAG agreement gave those companies a 24-day free rerun window. Hulu announced its first profitable quarters in 2010.

Also in 2010 (July 6), the first streaming deal with a massive price tag was announced, as Netflix and Relativity Media did a $100 million a year deal to bypass traditional pay tv and to go direct to Netflix after theatrical.

This event triggered every content owner that was being paid at significantly lower rates (which at the time was everyone) to withdraw their content as quickly as possible. Both Disney and Sony found ways out of their full agreement with Starz, which was the top provider of streaming studio movies to Netflix at the time.

Also in 2010, HBO Go launched with some films from the four studios with which they have output deals, but with more of an emphasis on the original HBO content library. And Hulu launched Hulu-Plus, which allowed subscribers to push some of their reruns to TVs, instead of just computers and phones/tablets, and slowly added some exclusive content.

Streaming, even at the high prices that Netflix was paying, could not replace the lost DVD revenue. But it was a new revenue stream that made the pain a little less dramatic.

But as these new services rolled out, there was actually less and less major studio content available to stream. Studios didn’t rebel against HBO. But when it came to Netflix or Hulu-Plus or eventually Amazon, etc, they want(ed) to get paid.

And looking at the broad strokes, we’re still there.

The EPIX streaming deal with Netflix includes Paramount and Lionsgate product, is non-exclusive and limited to films that are actually playing on the EPIX cbale/satellite network.

Warner Bros has its HBO relationship and has also built out the Warner Archive product for streaming. They also bought Flixter a few years back, which may ultimately be something or nothing. But the vast majority of their library is not available for streaming.

Sony owns Crackle, which has about 150 Sony library movies available at any time.

Disney has a $350 million deal with Netflix that starts next year, but it is unclear if there is much exclusivity outside of TV and there is still talk about Disney launching their own channel.

Fox and Universal have deals at HBO, but are floating a bit, though you can count on Universal’s strategy being heavily influenced by its parental relationship (Comcast).

To give you some perspective, there were nine Best Picture nominees 2 years ago, which puts us outside of their pay-tv windows. As of this writing, of those 9 Best Picture nominees, only 2 are available to stream via a subscription service, Django Unchained and Silver Linings Playbook, both on Netflix thanks to their deal with The Weinstein Company.

Think I am being snobby? Of the Top 10 grossers of that same year, only 2 are available on a subscription streaming service. Skyfall is on Netflix and Amazon Prime and Madagascar 3: Europe’s Most Wanted is currently available on FX Now (which is free with cable/satellite).

Of course, you can buy or rent any of these titles for as little as $2.99, but now we’re back to Blockbuster.

Consumers have shown, thanks to Netflix, that they are willing to pay for a subscription service so they can watch what they like when they like. But at this moment, that option isn’t on the table for most of the studio libraries. But it will be… because it has to be.

Why didn’t Blu-ray, once it got past HD DVD aka “Red-ray,” raise the bar for the sell-thru Home Entertainment business? Because as that fight was happening, cable/satellite was converting to HD and the vast majority of consumers couldn’t really see the difference between a Blu-ray disc and the cable/satellite delivery of the same film in HD or a stream… certainly not enough so they would pay $15+ for a Blu-ray disc. Yes, there is the cinephile market. I have my shelves loaded with Blu-ray. But, I haven’t bought a new one in quite a while. I get the Criterion Collection on Hulu-Plus. I have more to watch than I can handle.

Those libraries, thousands of titles deep, can’t just sit there gathering dust. They cry out for exploitation. A few years into streaming, a lot of the eggs have been unscrambled. Studios are much closer to being prepared to exploit those libraries in the new streaming/DVR-driven universe.

I don’t know the specifics of the Disney/Netflix deal, but I can say this… whoever can boast of being the exclusive streaming home of the Star Wars library has a huge advantage. Whoever can boast about being the exclusive streaming home of Pixar and Disney films has a huge advantage. As we critical types are gushing about “House of Cards” or “Transparent,” in the real world, there are 20 million homes that will choose to pay monthly for a subscription that will include a densely-packed subset of films that are beloved. And each studio has a library with that kind of muscle.

Will Disney give Netflix that advantage or will it build its own business? That is the mega-question of the next couple years.

In the cable era, it worked both ways. None of the other premium cable networks were ever able to match HBO’s subscriber base. But they sold movies to HBO and eventually, a few studios got together and built their own premium network, which was part of what drove HBO to shifting focus to more original programming.

But the key here is the library, not just the first wave of “pay-tv” revenue. None of it is getting more valuable sitting on the shelf. And for the first time in history, technology will allow content owners to make everything they own available to audiences at any time.

The questions are, what does the media experience look like for the consumer and how does the money pie get split up moving forward?

Those questions and more in Part 2: Meet The New Bundle. Same As The Old Bundle, Part 3: The Tyranny Of The Old, and Part 4: $200 Billion Is Never Enough.

2 Comments »Weekend Estimates by Premature Summerlation Klady

A mega-opening used to be a shocker. Now, not so much. We never saw a $100m opening before 2002’s Spider-Man. And since 2005, we haven’t had a year with fewer than two. In 2012, we had four. Three in 2013. Just two last year, leading to “sky is falling” stories that didn’t account for the massive budget tightening that made last year one of the best years for most of the studios, in terms of profit (oh, that!) ever. And now, our first $100m opener of 2015.

It’s interesting, looking at the chart, that Disney’s Marvel division is the superstar of Hollywood right now and they only have three $100 million openings. That might put opening-mania (brought to you by the breathless media) into perspective. Marvel will have its fourth $100m opening in four weeks, perhaps the second $200 million opening in history (after their own Avengers).

The other striking thing is how odd last year really was. For one thing, Transformers: Age of Extinction delivered the lowest overall domestic gross from a $100m+ domestic opening so far. $245 million after a $100 million launch.

But on the world stage, none of the three films that did over $300 million domestically did as much as $800 million worldwide. And two of the films in the mid 200s (Transformers and Hobbit) did over $950 million each. Even if one uses the China Asterisk (which we really should when discussing mega-grosses), Tranformers would still be over $900 million worldwide and Hobbit around $895m. (For me, the “China Asterisk™” is counting the China gross for American films at 50% the revenue value for the distributor/studio/producer of any other country’s gross. This is because only 20% of China theatrical grosses are returned to distributors, as opposed to about 45% for most foreign territories and 55% domestically.)

So are the 2014 numbers an anomaly, or the future? No one can really know. Our first $200 million domestic grosser of 2015 will be Furious 7 and it seems like a lock to do over $800 million worldwide. So that will end last year’s trend. Avengers 2 will do likewise.

For the last decade, big films with over 70% of the gross coming from international have been 36% of the cases (10 of 28). Of those 10, two Hobbits, two Ice Ages, a Pirates, and a Transformers (6 total) grossed less than $300m domestic. Bond, Hobbit 1, Potter 7a, and Avatar both broke $300 million domestically and $800m worldwide, suggesting the imbalance was less significant.

What strikes me is that we may be seeing with franchises very much what we saw with movie stars in years past. Perhaps it is not, as I have felt in the past, that the rest of the world is simply behind the U.S. on the trend line by three or four years (the fading of 3D being the next big landmark if that is the case). But rather – or in addition – that there are franchises that, somehow, just play better internationally than domestically.

Note – Almost all $500m+ worldwide grossers now gross more internationally than domestically. That’s not what I am talking about. I am talking about over 75% coming from international. Ice Age, the last Transformers, the last Pirates. Are these the Brad Pitts of current Hollywood?

Also… this is the one weak part of Marvel’s game, which you can be sure they are working on improving. They have had just two films of their ten – Avengers and Iron Man 3 – do over $460m internationally. This is not a dig at Marvel. But if things ever slide domestically, it is great to have international there as a safety net (or cash cow). Avengers did 59% of its business internationally. Someone with a slide rule is worrying today about getting that percentage – no matter how it does domestically – up to IM3‘s 66% or better. If they can do that, they can start projecting champagne baths for an extra couple of years.

Great opening by Furious 7. Impressive. And Furious 7 is a Top 10 all-time. (Seven of those 10, btw, are not 3D… for those who endlessly worry about 3D asterisk-ing stats.)

Not a whole lot else to chew on this weekend. Drops were modest, but nothing to write home about.

It Follows is not growing, even with added theaters. It has nothing to do with the movie. It has to do with marketing… or lack thereof. And that was a decision that came long before the (correct) choice to push VOD back. They should have never set the film with a day-n-date VOD. But we’re discussed that in depth before. VOD is great if you are aiming relatively low… and terrible for a movie that has real commercial appeal. (Kinda like my Old Harvey Weinstein thing… great cutter if your movie sucks, terrible cutter if your movie is great.)

While We’re Young added 7x the theater count and got a 2x bump. Still, it seems to be running more in line with bigger A24 films, rather than the smaller ones. One never knows, but $4m – $5m is looking doable for this one (which would make it Top 5 for A24).

21 Comments »Friday Estimates by Kladious 7

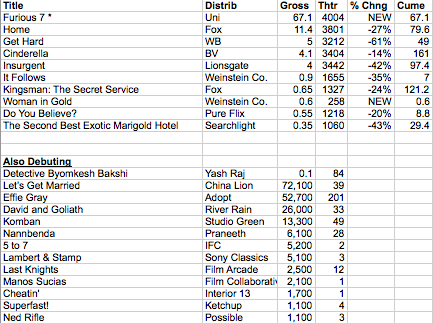

What can you give a movie that’s got it all?

After 7 movies, in which quality seems to be a minor detail, the Fast & Furious franchise is making its next great leap, it seems. The first film was a hit back when DVD drove the business and international was increasing… but the film wasn’t a big hit overseas. Tokyo Drift was an attempt at reaching out… and was the commercial low point of the series. But when they returned to the well, BOOM, 2009’s Fast & Furious not only had the highest domestic gross of the series, but it nearly doubled the previous best international gross. International doubled again for Fast Five. And it grew another 25% for Fast & Furious 6. Meanwhile, domestic crept up too. But based on this opening, Furious 7 should take at least a 30% leap over the last film here at home alone. That’s big. And if international follows, massive, threatening the billion dollar mark.

Now, it may turn out that this is just a massive front-loaded opening day. But… well… we’ll see…

Pretty much everyone else avoided this date. Harvey Weinstein grabbed a counter-programming slot to okay-ish results with Woman in Gold.

Home is holding well, more good news for Jeffrey Katzenberg.

Cinderella is holding even better, though Disney is probably a little less than thrilled that this one isn’t stronger, cash cow though it may be.

Insurgent continues to fall ever-so-slightly farther behind Divergent.

It Follows expands by 437 screens, but drops 35% from last Friday. It’s great that the hardcore showed up for the hardly-advertised film, but it’s difficlut to change course from a day-n-date opening. This is a success compared to what the numbers would have been with d-n-d, but a disappointment when you realize how this film might have done in a straight theatrical.

25 Comments »